What is a Unit Investment Trust?

Unit Investment Trusts (UITs) are exchange-traded mutual funds offering a fixed (unmanaged) portfolio of securities having a definite life. Investors should be aware that there are risks to investing in UITs. Unit Investment Trusts typically issue redeemable securities (or “units”), like a mutual fund, which means that the UIT will buy back an investor’s units at the investor’s request, at their approximate net asset value (NAV) . Typically, a UIT will make a one-time “public offering” of only a specific, fixed number of units (like closed-end funds).

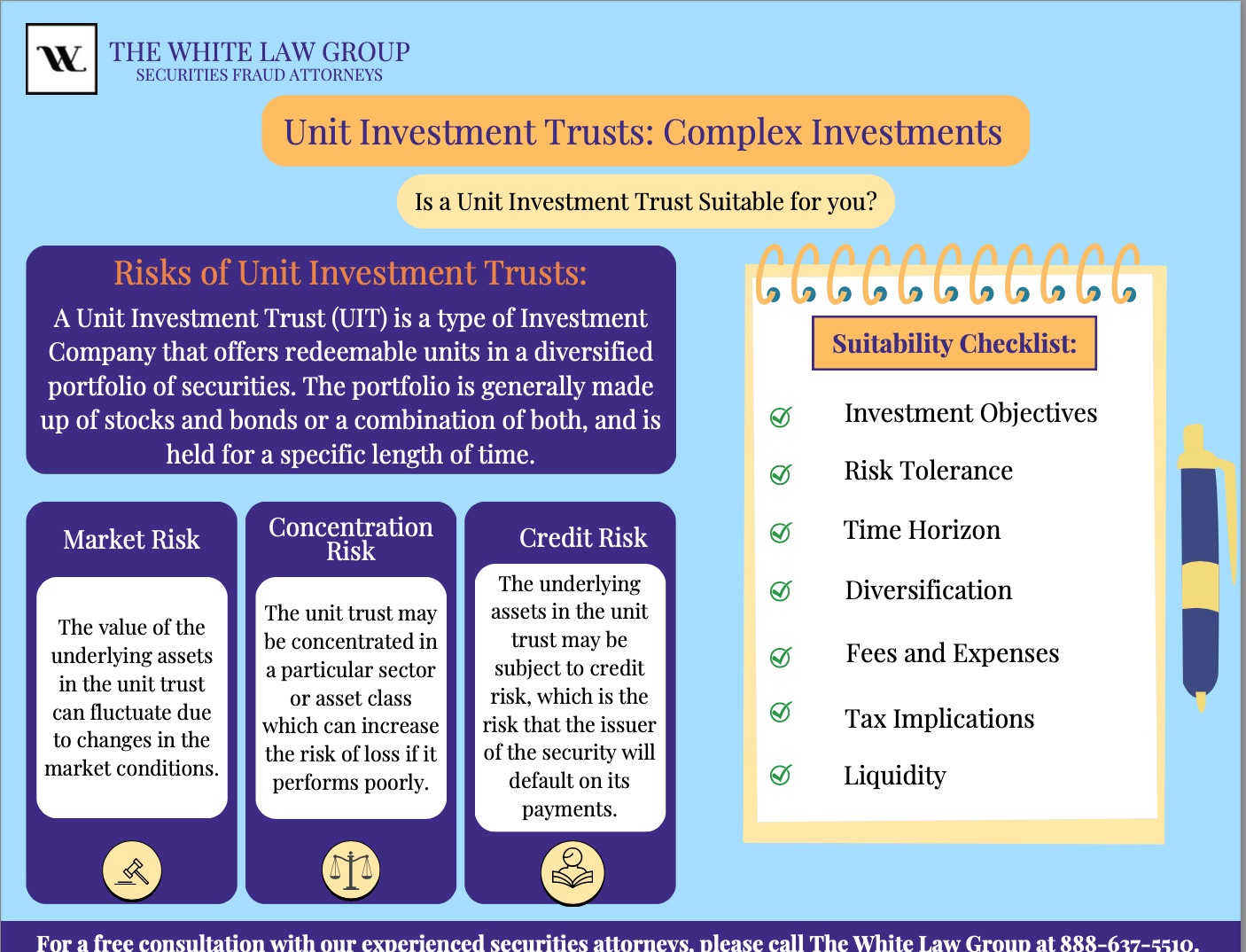

What are the Risks of Investing in Unit Investment Trusts?

Many UIT sponsors will maintain a secondary market, which allows owners of UIT units to sell them back to the sponsors and allows other investors to buy UIT units from the sponsors. Often, if units are bought back from the sponsor, it’s at a discounted rate, which means a loss for the investor. This can be problematic when the units are invested in volatile or risky sectors.

Many UIT sponsors will maintain a secondary market, which allows owners of UIT units to sell them back to the sponsors and allows other investors to buy UIT units from the sponsors. Often, if units are bought back from the sponsor, it’s at a discounted rate, which means a loss for the investor. This can be problematic when the units are invested in volatile or risky sectors.

UITS don’t actively trade their investment portfolio. That is, a UIT buys a relatively fixed portfolio of securities (for example, five, ten, or twenty specific stocks or bonds), and holds them with little or no change for the life of the UIT. Because the investment portfolio of a UIT is fixed, investors know basically what they are investing in for the duration of their investment. Unfortunately, if one of the securities is underperforming, no adjustments can be made. This is especially important in the volatile energy sector. Just because a UIT had excellent performance last year does not necessarily mean that it will again this year.

Unit Investment Trusts (UITs) have a termination date that is established when the UIT is created. When a UIT terminates, any remaining investment portfolio securities are sold and the proceeds are paid to the investors. Many brokers are pushing “short-term strategy” trusts that dissolve after one to two years, possibly because of the high transaction fees, which are charged with the purchase and again with the dissolution. UITs can be very attractive to brokers due to the high upfront commissions, usually around 4%.

On behalf of investors, The White Law Group is investigating claims that some brokers violated securities law and FINRA regulations when selling certain UITs. It’s possible the broker-dealers failed to perform adequate due diligence on the UITs before offering them for sale to their clients and that the brokerage firms failed to determine whether the investments were appropriate in light of their clients age, investment, experience, net worth, and tolerance for risk. If a broker overlooks suitability requirements, investors may have an actionable claim to recover their losses in a product in a claim through FINRA dispute resolution.

Examples of Unsuitable Unit Investment Trusts:

On March 1, 2023 financial advisor Gary Bowman allegedly failed to file an Answer to CFP Board’s Complaint within the required timeframe. The CFP Board’s Complaint was in connection to allegations by the Financial Industry Regulatory Authority (FINRA), in which Bowman was suspended from association with any FINRA member in any capacity for three months. Bowman was issued a $10,000 fine for violating FINRA Rules 2111 and 2010. According to FINRA, Bowman was accused of engaging in unsuitable patterns of short-term trading of Unit Investment Trusts (UIT) in customer accounts. Additionally, Bowman was purportedly making recommendations that caused his customers to incur avoidable sales charges. FINRA also alleges that the frequency and cost of these transactions were unsuitable.

On October 20, 2015 The Financial Industry Regulatory Authority (FINRA) announced that it ordered 12 firms to pay restitution totaling more than $4 million and fines totaling more than $2.6 million for failing to apply available sales charge discounts to customers’ purchases of Unit Investment Trusts (UITs), and related supervisory failures. A Unit Investment Trust (UIT), composed of redeemable units of fixed portfolio of securities, are risky due to their fluctuations based on the market. Sponsors generally offer sales charge discounts to investors, known as “breakpoint discounts” and “rollover and exchange discounts.” In March 2004, FINRA issued a Regulatory Notice to firms titled, Unit Investment Trust Sales, to remind broker-dealers that they should develop and implement procedures to ensure customers receive appropriate sales charge discounts for UITs.

Suitability Checklist for Unit Investment Trusts

Your financial advisor should only recommend investments that are suitable for you. Liquidity needs, time horizon, risk tolerance, age, income, are just a few categories an advisor should take into account prior to recommending any investment. Once that is completed the brokerage firm must ensure that due diligence was completed at every level of each investment. Here are some questions to ask when thinking about investing in Unit Investment Trusts (UITs):

- Investment Objectives: Does the UIT align with your investment objectives?

- Risk Tolerance: Do you have the risk tolerance to invest in a UIT?

- Time Horizon: Do you have a long enough time horizon to hold the UIT until maturity?

- Diversification: Does the UIT provide adequate diversification for your portfolio?

- Fees and Expenses: Are the fees and expenses associated with the UIT reasonable and appropriate for your financial situation?

- Tax Implications: Are the tax implications of investing in the UIT appropriate for your tax situation?

- Liquidity: Do you have the liquidity needed to hold the UIT until maturity?

- Suitability of Underlying Assets: Are the underlying assets of the UIT suitable for your investment objectives and risk tolerance?

Investors may have grounds to file an actionable claim through FINRA dispute resolution to recover their losses in a product if a broker fails to comply with suitability requirements.

What is FINRA Arbitration and How Does it Work?

Financial Industry Regulatory Authority (FINRA) is the regulator who oversees brokers and brokerage firms. If you feel you have been defrauded you may be able to seek restitution through FINRA arbitration. Once you’ve retained a securities fraud attorney, the process of filing a claim through FINRA could take place. This claim should include a description of the fraud, the amount of money lost, and any supporting documentation. Once the claim is filed, FINRA will appoint an arbitrator to hear the case. The arbitrator is responsible for reviewing the evidence and making a decision about whether the investor is entitled to restitution. If the arbitrator rules in favor of the investor, they will issue an award for damages, and this can be used to seek restitution from the person or company that defrauded the investor. FINRA is overseen by the Securities and Exchange Commission (SEC) and is authorized by Congress to protect U.S. investors from investment fraud by making sure the broker-dealer industry operates fairly and honestly.

Do I Need a Securities Fraud Attorney?

If you have questions about your investment in a UIT and would like to speak to a securities attorney about your potential to recover losses through FINRA arbitration, please call The White Law Group at 1-888-637-5510 for a free consultation.

The White Law Group, LLC is a national securities fraud, securities arbitration, investor protection, and securities regulation/compliance law firm with offices in Chicago, Illinois and Seattle, Washington. For more information on our firm, please visit our website: https://whitesecuritieslaw.com/

Tags: Unit Investment Trusts Last modified: July 24, 2023